“History teaches that economic slowdowns rarely emerge overnight. They often begin with subtle signals: weakening consumption, slower business activity, declining tax collections, reduced investment enthusiasm, and increasing caution among consumers and enterprises. Individually, these indicators may appear manageable. Collectively, they can point toward emerging economic headwinds.”

Recent economic data released by Indian government agencies has triggered fresh debate about the true state of the Indian economy. While official narratives continue to emphasize India’s position as one of the world’s fastest-growing major economies, certain underlying indicators suggest that policymakers, economists, and citizens alike may need to pay closer attention to emerging signs of economic stress.

Among the developments attracting attention is the reported sale of more than 7.6 tons of gold by the Reserve Bank of India (RBI) during May 2026. According to available reports, the value of these transactions exceeded $12 billion. While central banks routinely manage their reserves through purchases and sales of various assets, the scale and timing of such transactions inevitably invite questions regarding their purpose and implications.

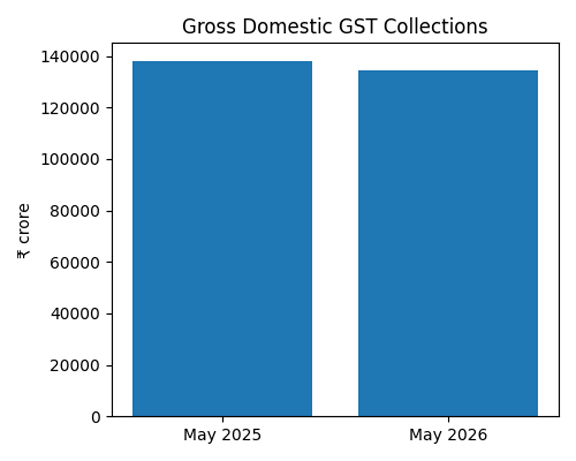

Equally noteworthy is the latest Goods and Services Tax (GST) data. Gross domestic GST collections, excluding Integrated GST (IGST) on imports, declined by 2.6 percent in May 2026 compared with the corresponding month in 2025. Domestic collections fell from ₹1,38,102 crore in May 2025 to ₹1,34,530 crore in May 2026.

A closer examination of the figures reveals a mixed picture.

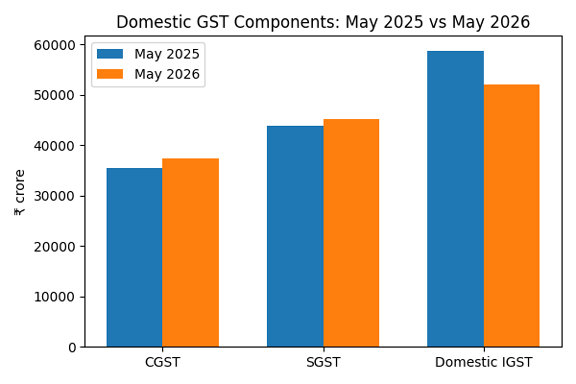

Central GST (CGST) collections increased by 5.5 percent, rising from ₹35,434 crore to ₹37,397 crore. State GST (SGST) collections also registered a modest increase of 2.8 percent, growing from ₹43,902 crore to ₹45,143 crore.

The most striking figure, however, is the performance of domestic IGST collections. These fell sharply by 11.4 percent, declining from ₹58,767 crore in May 2025 to ₹51,990 crore in May 2026.

Why does this matter?

Domestic IGST is generated largely through inter-state trade and business transactions. A significant decline in this component may indicate slowing commercial activity, weaker supply-chain movement, reduced consumer demand, or cautious business sentiment. While one month’s data does not establish a trend, the magnitude of the decline warrants attention.

Economists often caution against drawing sweeping conclusions from a single set of monthly figures. Tax collections can be influenced by timing issues, compliance adjustments, refunds, base effects, and administrative changes. Nevertheless, when multiple indicators begin moving in the same direction, they deserve careful examination.

The broader concern is whether India’s headline growth figures are masking weakness in sectors that directly affect ordinary citizens. For many households, the lived economic experience is shaped not by aggregate GDP statistics but by employment opportunities, wage growth, purchasing power, business profitability, and consumer confidence.

Across various sectors, there have already been reports of uneven consumption patterns. Premium consumption among affluent households has remained relatively strong, while demand in several mass-market categories has shown signs of moderation. Such divergence often suggests that economic growth is becoming increasingly concentrated rather than broad-based.

Small and medium enterprises, which constitute the backbone of India’s employment structure, continue to face multiple challenges, including rising compliance costs, competitive pressures, access to affordable credit, and fluctuating consumer demand. If inter-state trade activity is indeed slowing, these businesses are often among the first to feel the impact.

The reported RBI gold sale adds another dimension to the discussion. Central banks buy and sell gold for numerous legitimate reasons, including portfolio rebalancing, reserve diversification, liquidity management, and risk mitigation. Therefore, the sale itself should not automatically be interpreted as evidence of economic distress.

However, transparency is critical in maintaining public confidence. Whenever significant reserve-management decisions occur, clear communication helps prevent speculation and reassures markets. In the absence of adequate explanation, observers naturally seek connections between reserve actions and other economic developments occurring simultaneously.

The timing of substantial gold sales alongside softer domestic GST collections has therefore raised questions among analysts. Are policymakers responding to temporary liquidity requirements? Are they managing external financial pressures? Or are these unrelated developments occurring independently?

At present, definitive answers remain unavailable.

What is clear is that India faces a challenging global economic environment. Growth across many advanced economies remains subdued. Geopolitical tensions continue to disrupt trade flows. Energy prices remain vulnerable to international developments. Financial markets worldwide are adjusting to changing interest-rate expectations and shifting investment patterns.

Against this backdrop, India has demonstrated considerable resilience. Infrastructure investment remains strong, digital transformation continues at an impressive pace, and the country retains significant long-term growth potential driven by demographics, entrepreneurship, and technological innovation.

Yet resilience should not breed complacency.

History teaches that economic slowdowns rarely emerge overnight. They often begin with subtle signals: weakening consumption, slower business activity, declining tax collections, reduced investment enthusiasm, and increasing caution among consumers and enterprises. Individually, these indicators may appear manageable. Collectively, they can point toward emerging economic headwinds.

The decline in domestic GST collections, particularly the sharp fall in domestic IGST, should therefore be viewed neither as a cause for panic nor as a statistic to be dismissed. Rather, it should serve as an invitation for deeper scrutiny.

Policymakers would be well advised to monitor demand conditions closely, support productive investment, strengthen job creation, and ensure that growth benefits reach a broader section of society. Sustained economic expansion ultimately depends on robust consumption, healthy business activity, and widespread public confidence.

India remains one of the world’s most promising economies. The country possesses immense human capital, entrepreneurial energy, and institutional strengths. However, maintaining momentum requires vigilance, transparency, and a willingness to confront emerging challenges honestly.

The question before policymakers and citizens alike is not whether India possesses the capacity for continued growth—it undoubtedly does. The real question is whether the latest economic signals represent temporary fluctuations or the early warning signs of a broader slowdown.

The coming months will provide the answer. Until then, prudence demands careful observation rather than complacent celebration.

(Dave Makkar is a New Jersey, US -based social activist and writes on economy and community. He an be reached at davemakkar@yahoo.com)

Be the first to comment